What Is a Bear Put Spread? | Beginner's Guide

Bear put spreads explained visually: payoff diagrams, Greeks tables, and examples showing how the strategy works.

A bear put spread, or put debit spread, combines buying a put at a higher strike and selling a put at a lower strike, same expiration, same underlying. This moderately bearish strategy has defined risk and limited profit potential. It’s one of the four vertical spreads (two strike prices, one expiration).

Bear put spreads work best when you’re bearish and expect the stock to move lower to a specific price.

With the stock at $500, an example bear put spread would be:

- Buy one 500 put at $30

- Sell one 450 put at $12

- Net Debit: $18

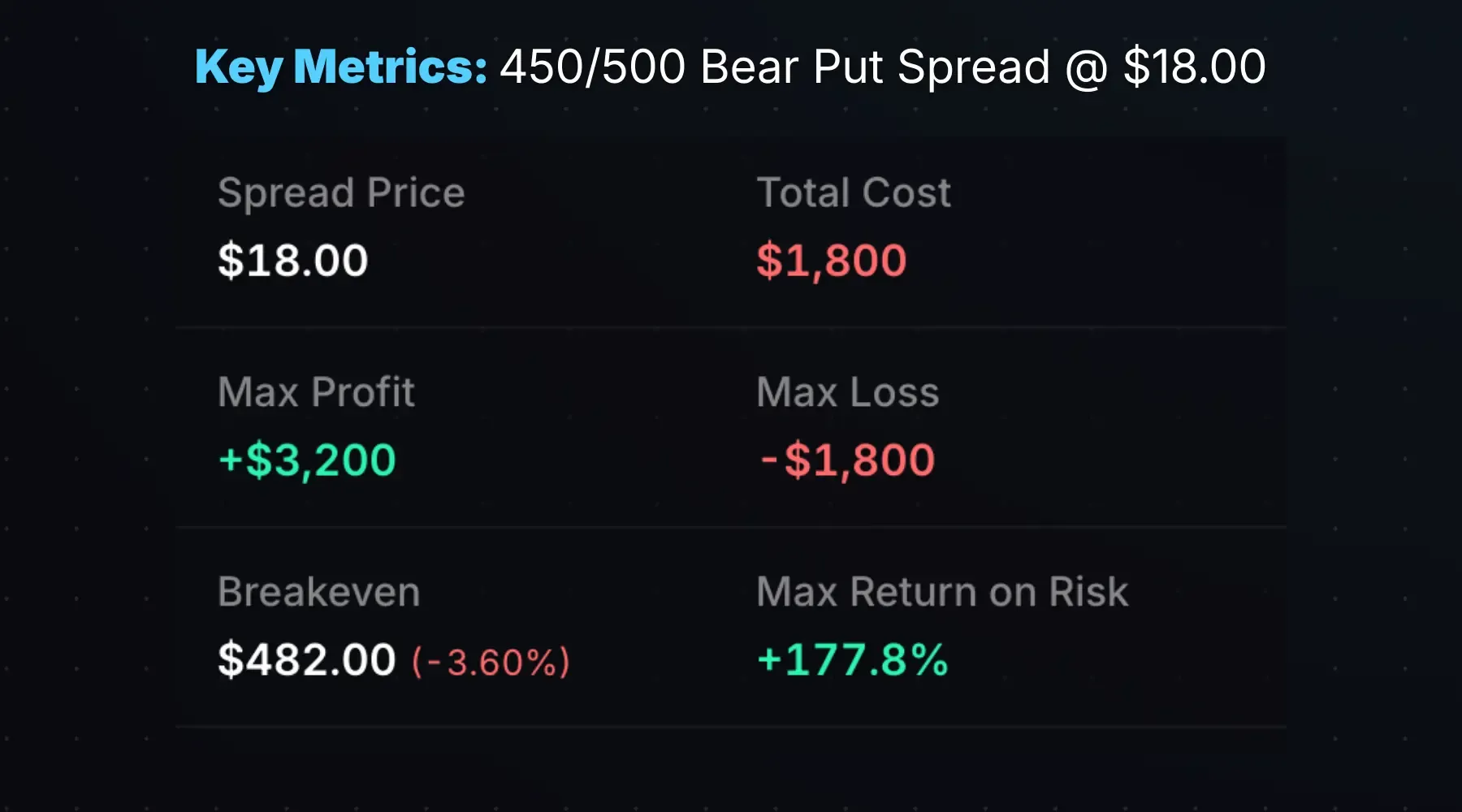

Resulting Position: a 450/500 bear put spread entered for a net debit of $18.

Buying the 500 put on its own costs $30, while buying this put spread costs $18. This reduces the cost and risk of the trade, and raises the breakeven price.

Payoff Diagram

The bear put spread payoff diagram has defined risk on the upside, and limited profit potential on the downside:

Stock at Entry: $500. Trade: 450/500 put spread entered for an $18.00 net debit. 45 days to expiration (DTE).

The white line shows the payoff at expiration. The max loss of $1,800 occurs if the stock price is at or above the long put strike of $500. The max profit of $3,200 occurs if the stock price is at or below the short put strike of $450.

The cyan line (T+0) shows the payoff right now (entry in this case). Profits and losses are muted before expiration because both options still have extrinsic value. Max profit/loss only occurs when extrinsic value is gone, which is the case at expiration.

Key Characteristics

- Max Profit: (Spread width − net debit) × 100 × number of spreads

- Max Loss: Net debit × 100 × number of spreads. Occurs if the stock closes at or above the long put strike at expiration.

- Breakeven: Long put strike − net debit

- Outlook: Moderately bearish

Here are the metrics for a 450/500 put spread purchased for an $18.00 net debit:

- Max Profit: $3,200 (spread width of $50 − $18 net debit = $32 × 100)

- Max Loss: $1,800 (net debit × 100)

- Breakeven: $482 (long put strike − net debit)

- Max Return on Risk: +177.8%

Achieving the max profit requires the stock to be $450 or lower at expiration, a 10% drop, but a 177.8% return on the put spread. At $482 (breakeven), the spread value equals the entry cost.

How the Greeks Affect a Bear Put Spread

Bear put spread Greeks can change: gamma, theta, and vega flip depending on where the stock is relative to the strikes.

| Greek | Near Long Strike | Near Short Strike |

|---|---|---|

| Delta (Δ) | Negative | Negative |

| Gamma (Γ) | Positive | Negative |

| Theta (Θ) | Negative | Positive |

| Vega (ν) | Positive | Negative |

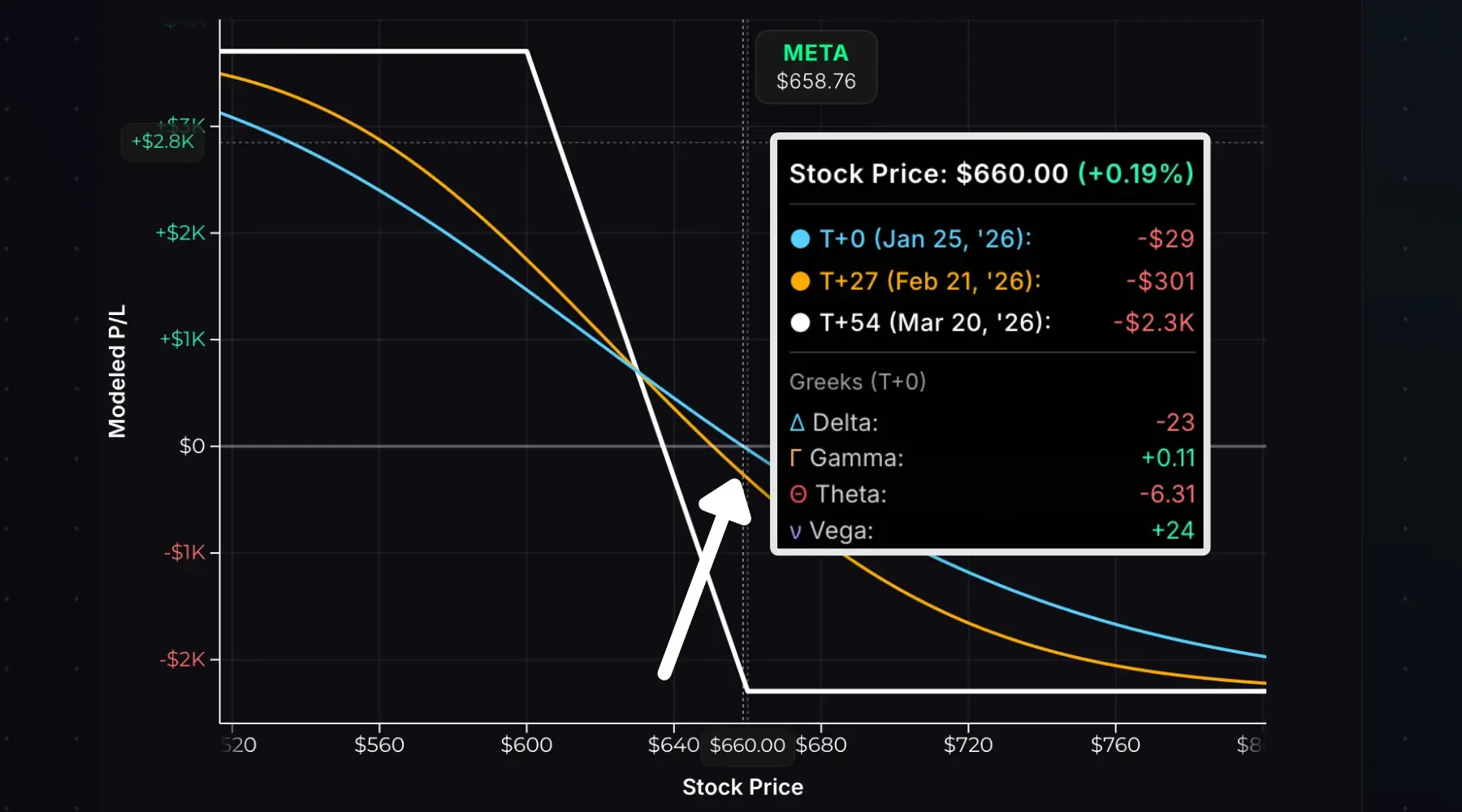

Here’s a 600/660 bear put spread on META with the stock near the long put strike ($660):

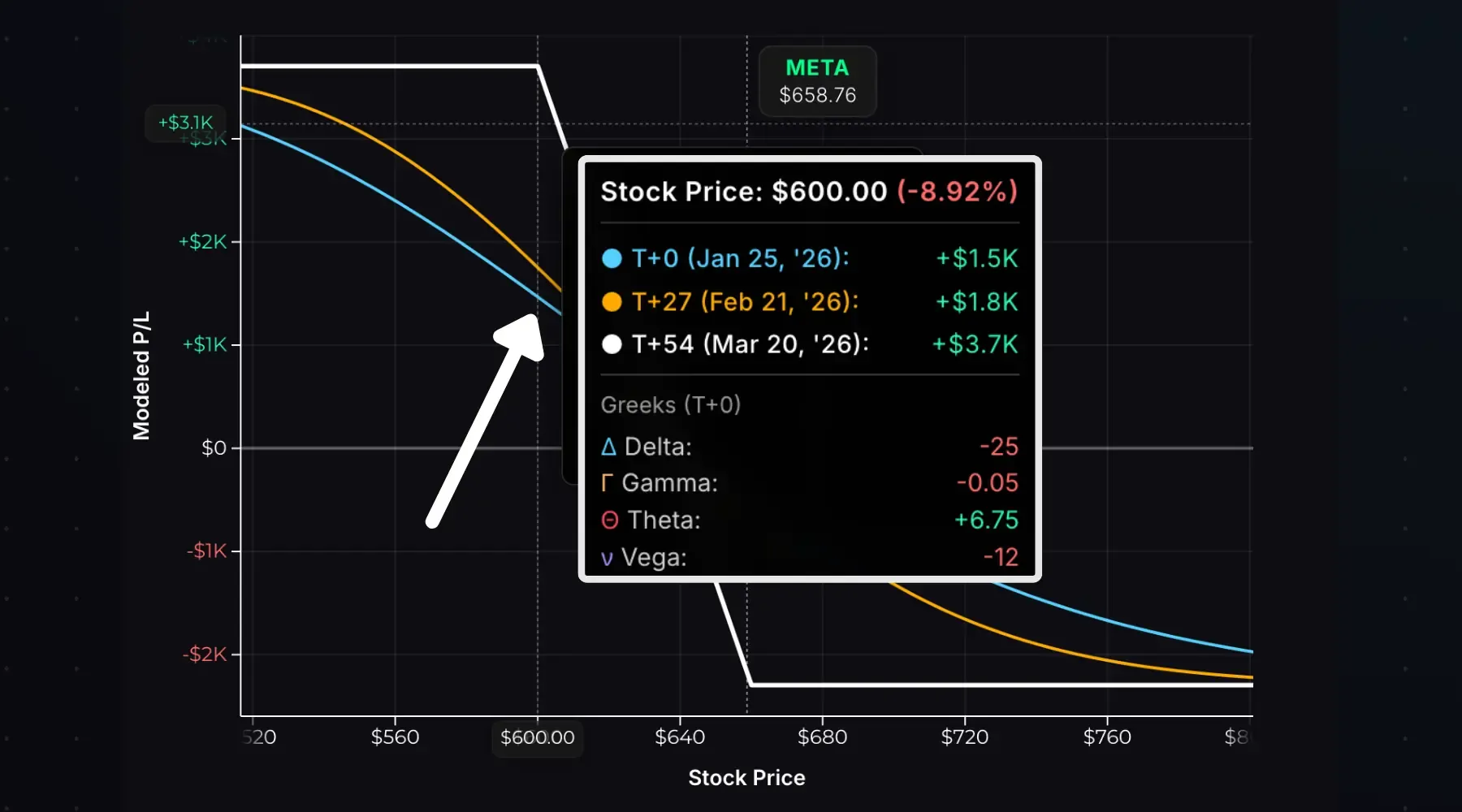

And with the stock near the short strike ($600):

You can see the Greeks by comparing the T+0 P/L line to the expiration P/L line (T+54 in the images):

- Near the long strike: T+0 is above the expiration P/L, so losses grow as time passes (negative theta). Rising implied volatility (IV) helps because the ATM long put has higher vega than the OTM short put.

- Near the short strike: T+0 is below expiration P/L, so profits grow as time passes (positive theta). Falling IV helps because the ATM short put loses more extrinsic value than the ITM long put.

A common claim is that “debit spreads are ideal when IV is low,” implying rising IV helps. This is misleading. If the stock moves in your favor toward the short strike, you want IV to fall, not rise.

Time Decay

Unlike a naked long put, a bear put spread has partially offsetting theta. The long put decays against you while the short put decays in your favor.

When the stock is near the long strike, net theta is negative, and time works against you. As the stock falls to the short strike, net theta flips positive, and time works for you.

This makes bear put spreads more forgiving than naked long puts if the stock price stagnates.

Choosing Strike Prices

Strike price selection affects the cost, risk/reward, breakeven, and probability of profit of a put spread.

Consider three $50-wide put spreads on a $500 stock with 45 DTE and 30% IV:

| Spread | Net Debit | Max Loss | Max Profit | Breakeven | Max Return |

|---|---|---|---|---|---|

| 475/525 (ITM) | $24.66 | $2,466 | $2,534 | $500.34 (+0.07%) | 102.8% |

| 450/500 (ATM) | $15.73 | $1,573 | $3,427 | $484.27 (−3.15%) | 217.9% |

| 400/450 (OTM) | $3.46 | $346 | $4,654 | $446.54 (−10.7%) | 1,345.1% |

The ITM spread costs the most since you’re buying intrinsic value in the ITM put, but has the highest breakeven: the stock can stay flat and the position will make $34. The max return is 102.8%, risking $2,466 to make $2,534. The spread hits max profit if the stock falls to or below $475 at expiration.

The OTM spread costs the least, but has the lowest breakeven: the stock must fall 10.7% by expiration. The max return is 1,345.1%, risking $346 to make $4,654, but it’s a low probability bet. The spread only hits max profit if the stock is down 20%+ at expiration, and loses the full cost if the stock doesn’t fall at least 10%.

Key Insight: Pushing strikes further OTM increases risk/reward, but lowers the breakeven and reduces the probability of profit.

-

ITM Spreads: higher probability, lower payoff.

-

OTM Spreads: lower probability, higher payoff.

Use the bear put spread calculator to model different strike combinations.

Choosing an Expiration

A bear put spread’s max profit occurs when both options lose all extrinsic value, typically at expiration. This means even when a spread is fully ITM, you won’t see the max profit until time decay does its work.

Shorter-Term Spreads: When the spread goes ITM, theta flips positive and works quickly in your favor. You’ll approach max profit faster.

Longer-Term Spreads: Even when fully ITM, most of the max profit is locked up in extrinsic value. You’ll need to wait for time decay to eat away at extrinsic value, and waiting longer means the stock might turn higher and render your spread unprofitable.

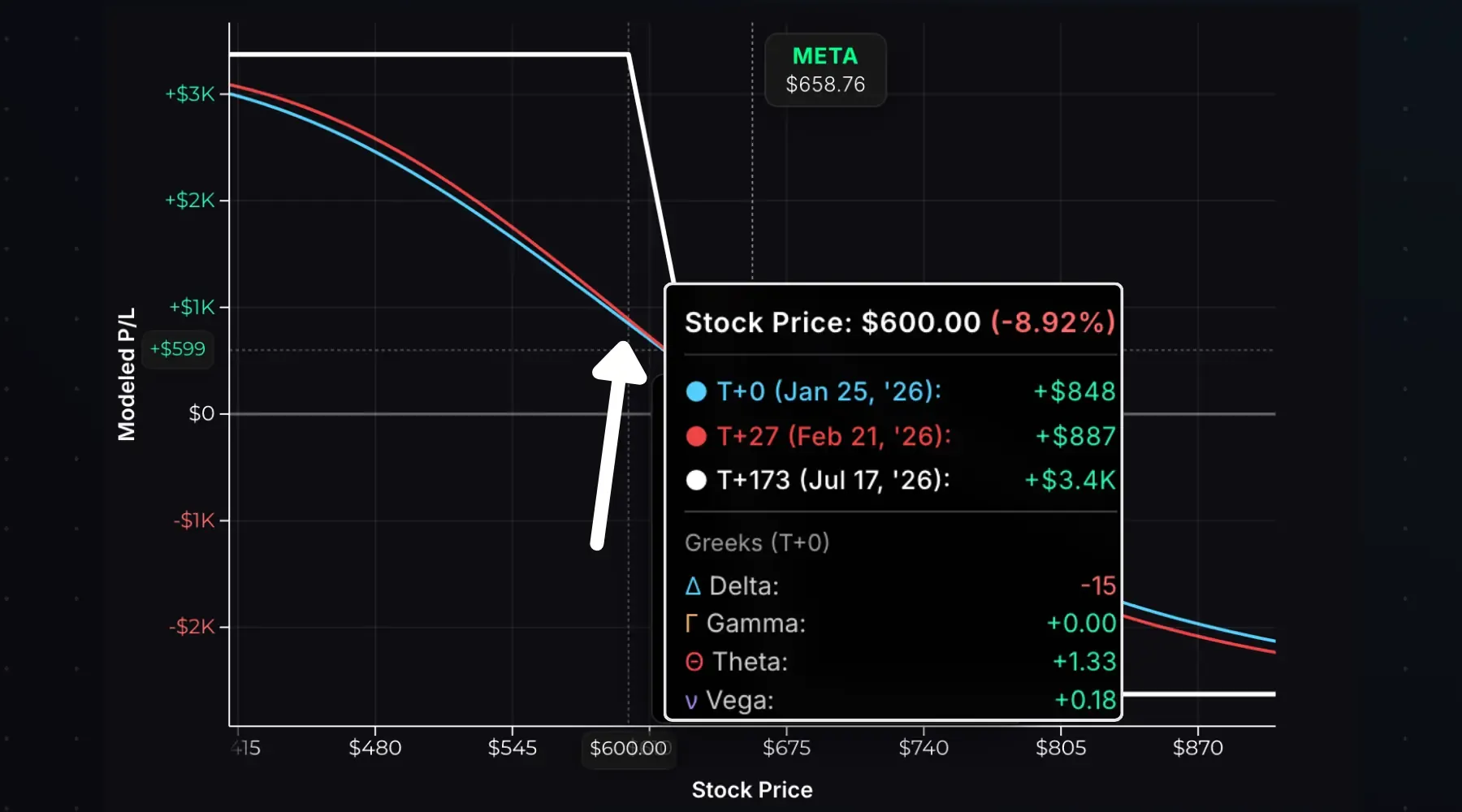

Consider a 54 DTE 600/660 put spread on META. If META drops to $600 immediately after entry:

The spread shows +$1,500 profit with theta at +6.75, or 41% of max profit captured.

Now consider the same 600/660 put spread and move lower, but with 174 DTE:

Same strikes, same $60 move, but only an $848 profit and theta at +1.33.

Here’s the comparison:

| Metric | 54 DTE Spread | 174 DTE Spread |

|---|---|---|

| Modeled Profit | +$1,500 | +$848 |

| % of Max Profit | 41% | 25% |

| Theta | +6.75 | +1.33 |

The 54 DTE spread captures more of the max profit; the 174 DTE spread captures less. Longer-term traders with fully ITM put spreads must wait longer to see max profit, and that’s if the spread remains ITM.

Bear Put Spread vs Long Put

A put spread costs less than a naked put using the same long strike price, and that lower cost dramatically improves the return profile.

Consider a $100 stock:

| Position | Entry Cost | Breakeven |

|---|---|---|

| Long 100 Put | $8.00 | $92.00 (−8.0%) |

| Long 90/100 Put Spread | $5.00 | $95.00 (−5.0%) |

The spread costs less and has a higher breakeven. Here’s what that means for the return profile of the spread vs. naked put:

| Stock Price | Put Profit | Spread Profit | Put Return | Spread Return |

|---|---|---|---|---|

| $100 | −$8.00 | −$5.00 | −100% | −100% |

| $95 | −$3.00 | $0 | −37.5% | 0% |

| $92 | $0 | +$3.00 | 0% | +60% |

| $90 | +$2.00 | +$5.00 | +25% | +100% |

| $85 | +$7.00 | +$5.00 | +87.5% | +100% |

| $80 | +$12.00 | +$5.00 | +150% | +100% |

Green highlights show the winning strategy at each stock price.

At $90 (a 10% move lower), the long put returns 25% while the spread returns 100%.

Key Insight: The spread outperforms the long put unless the stock price plummets (20%+ in this case). For most bearish scenarios, the spread wins on capital efficiency.

Early Assignment

The short put in your spread can be assigned early, but this isn’t a concern for bear put spreads. If your short put is assigned, the spread is already at or near max profit. You simply exercise your long put to sell the shares, locking in the spread width. Or, sell the long put and the shares in the same closing transaction to unwind the trade.

Entry, Exit, and Expiration

To enter: Place a spread order to buy the higher strike put and sell the lower strike put simultaneously. You’ll pay a debit to enter the trade.

To exit before expiration: Close the spread by selling the long put and buying back the short put as a single spread order. You’ll receive a credit when exiting the trade.

If you hold the spread through expiration:

| Scenario | Stock Price | Result |

|---|---|---|

| Both OTM | ≥ Long strike | Both puts expire worthless. Max loss. |

| Partially ITM | Between strikes | Long put exercises, short put expires. You sell/short 100 shares per put. |

| Fully ITM | ≤ Short strike | Long exercised and short assigned, net zero shares. Max profit. |

Using a 90/100 put spread entered for $3.00:

- Stock at $105: Both puts expire worthless. You lose the $300 entry cost.

- Stock at $95: Long put auto-exercises (sell/short shares at $100). Short put expires. You’re short 100 shares at a $97 effective sale price (long strike − debit).

- Stock at $85: Long put auto-exercises, short put gets assigned. You sell 100 shares at $100 and buy at $90, a $1,000 gain on the shares, minus the $300 entry cost = $700 net profit.

Avoid the partially ITM scenario. If only the long put expires ITM while the short expires OTM, you’ll be short shares and have significant upside risk instead of the defined-risk spread you started with.

- A bear put spread is a moderately bearish strategy with defined risk and limited profit potential.

- Max loss = net debit × 100 × number of spreads. Max profit = (spread width − net debit) × 100 × number of spreads. Breakeven = long put strike − net debit.

- Gamma, theta, and vega flip as the stock moves from the long strike to the short strike.

- ITM spreads have higher probability but lower reward; OTM spreads have lower probability but higher reward.

- Bear put spreads outperform long puts return-wise unless the stock moves explosively lower.

- Early assignment on the short put isn’t a problem. Exercise your long put and receive the spread width (max profit achieved).

- A bear put spread is a moderately bearish strategy with defined risk and limited profit potential.

- Max loss = net debit × 100 × number of spreads. Max profit = (spread width − net debit) × 100 × number of spreads. Breakeven = long put strike − net debit.

- Gamma, theta, and vega flip as the stock moves from the long strike to the short strike.

- ITM spreads have higher probability but lower reward; OTM spreads have lower probability but higher reward.

- Bear put spreads outperform long puts return-wise unless the stock moves explosively lower.

- Early assignment on the short put isn’t a problem. Exercise your long put and receive the spread width (max profit achieved).

Related Guides

- What Is a Long Put?: The building block of this strategy

- What Is a Bear Call Spread?: Credit spread alternative

- What Is Delta?: How option prices change with the stock price

- What Is Theta?: Understanding time decay

Ready to model your own spreads? Use our Bear Put Spread Calculator to visualize P/L for any strike combination.